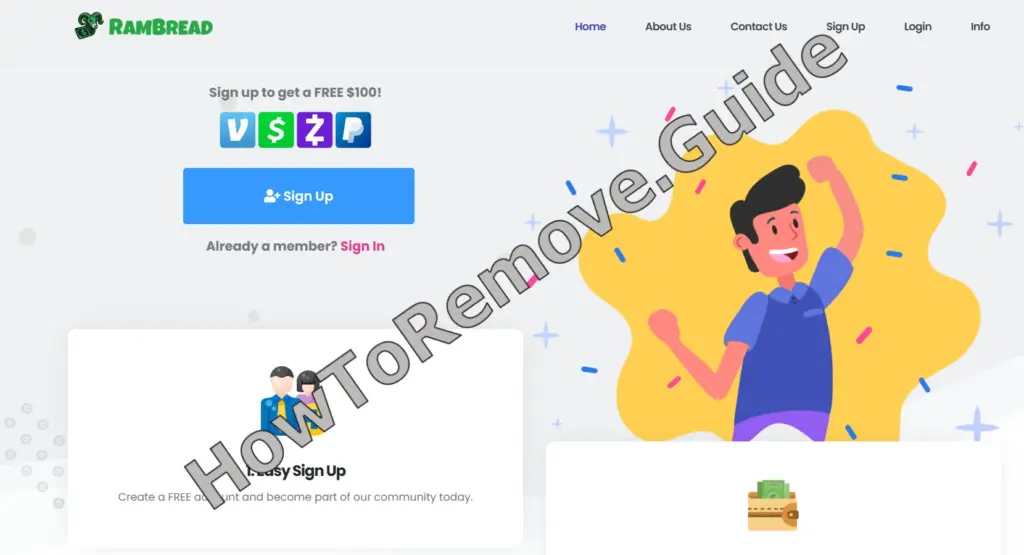

Did you just see a post promising a FREE $100 the moment you sign up, with extra cash for every friend who clicks your link? If the page was RamBread – also showing up as rambread.com, ref.rambread.com,RamStash or RamBucks – pause. Don’t rush to register, don’t hand over details, and don’t start blasting that link across your feeds. The pitch is dressed in big numbers and bigger promises, but the engine underneath runs on urgency, hype, and the idea that you’ll do the advertising for them.

Scams of RamBread.com‘s type are known to steal personal data and passwords. Install SpyHunter Pro to scan for risks, remove any dangerous trackers, and enable real-time protection.

Try Free For 7 Days*

Buy now15% OFF if you buy straight without trial.

Is RamBread Legit?

Here’s how the script usually unfolds. Bright banner. Big button. The claim that you’ll “Make Money Through Facebook, Instagram, SnapChat, TikTok, X.” You’re told advertisers pay the platform to reach “influencers,” and you’ll earn dividends based on your “influential power.” Then the counters roll in like drums: hundreds of thousands of “members,” millions “paid,” hundreds of thousands of “payments made.” It looks impressive at a glance. That’s the point. The promise is simple: easy sign up, earn from home, cash out through PayPal, CashApp, Venmo, or Zelle. It’s a frictionless fantasy – until you look at the seams.

A quick reputation check flagged the lowest possible trust score – one out of one hundred – and the domain was reported as freshly minted at the time of review, literally one day old. Think about that. A site that supposedly paid out millions but just registered? That mismatch is your first siren. Add the lack of real contact channels – no service email, no phone, no chat – and ownership hidden behind a WHOIS privacy service, and you’re staring at a profile that doesn’t square with a serious operation handling real payouts.

Now the money talk. You’ll see a FREE $100 for joining. You’ll see $50 per referral, $2 per click, and 20% from referrals. Ask yourself who can afford to pay that for random signups and stray clicks. Short answer: no one acting legitimately. Those giant counters – 300,543 members, $9,764,893 paid, 500,949 payments made, sometimes shown with plus signs – appear without verifiable support. The “testimonials” lean on first names and vague praise, not identities with proof. Meanwhile, threads that hype the same headline claims go silent when someone asks the only question that matters: did anyone actually cash out?

Here’s the part most people miss. The registration form asks for a full name, a username, an email, and a password. That’s already valuable. Layer on an expansive privacy text that discusses cookies, device identifiers, location data, and sharing with “Trusted Service Providers,” and the imbalance grows. Then comes the “Fraud Policy” – a long list of disqualifiers: VPNs, automation, buying traffic, buying referrals, self-referrals, “fake stats.” On paper it sounds protective; in practice it provides a ready-made pretext to deny withdrawals by declaring normal activity “inauthentic.”

Zoom back to the choreography. First, the FREE $100 hook. Then nudges to invite friends everywhere – Facebook, Instagram, SnapChat, TikTok, X, even Reddit. Your feeds become a distribution network, and your credibility becomes the lure. The big counters and big payouts make sharing feel safe. It isn’t. That pressure to spread is the system’s fuel, not a side effect.

Victim Experiences

Concrete experiences seal the pattern. One participant pushed hard for a day, saw two referrals credited, then watched a third and a fourth disappear. The dashboard balance? $304. The withdrawal? Blocked. Questions? Unanswered. Support? A ghost. Another telling detail: the dashboard showed a referral count but not names or emails of the referred users. Without that transparency you can’t verify anything. That’s a design choice, not a glitch, and it dovetails perfectly with the policy language built to accuse users of “fake stats” whenever a payout request hits the queue.

You might be thinking, “But there are long legal pages and corporate-sounding labels – doesn’t that mean it’s legit?” No. The dense text is there, yes. There’s even a postal address for privacy mail – P.O. Box 70, Manhattan Beach, CA 90267, Attention: Privacy – and talk of arbitration, U.S. and Canada coverage, and consumer-rights language. None of that repairs the operational holes: hidden ownership, no practical support, no verifiable payout trail, and counters that contradict a domain reported as brand new. Legal varnish doesn’t transform theater into evidence.

What to Do If You’ve Fallen for the RamBread Scam

What if you already stepped in? First, take control of what you can control. If you reused your password anywhere, change it now and make it unique. Turn on two-factor authentication for your email and financial apps. If you linked or planned to cash out through PayPal, CashApp, Venmo, or Zelle, review authorizations and recent activity. If you entered card details anywhere in the chase for a bonus, call your bank or card issuer and lock it down.

Second, preserve evidence. Screenshot the counters, the $100 signup banner, the “$50 per referral” language, your referral totals, and any error messages. Keep the exact links you used: the main domain, the referral subdomain, and any variants. If you posted your referral link, list where you shared it and remove those posts so others don’t get pulled in. Documentation turns a frustrating experience into a clear, actionable report.

Third, report. Flag the post where you found the pitch. On social platforms, report the promotion as a scam or deceptive offer. In your email client, mark messages pushing it as spam or phishing. When you file an incident report, include the domains, the payout claims, the lack of contact options, the hidden ownership, the one-out-of-one-hundred trust signal, and the fact of blocked withdrawals. Be specific and factual. Vague reports fade; details travel.

Recognizing Warning Signs Specific to RamBread

Let’s break down the persuasion playbook so you can spot it faster next time. Quoted promises – “FREE $100,” “$50 per referral,” “assured payments daily” – are signals, not facts. Giant counters are set pieces unless they come with verifiable proof. Name-dropping payment apps borrows legitimacy without providing it. Long legal pages act like costumes, not accountability. And that anti-fraud page? It’s a maze of disqualifications that can be invoked whenever money needs to be withheld.

Remember the timeline cue. A domain reported as one day old paired with “millions paid” is like hearing a newborn brag about a decades-long career. When age and achievement don’t rhyme, you move on. Also watch for the social-proof loop: posts that repeat headline numbers and referral bounty but go quiet around withdrawals. Real payouts come with receipts, not silence.

One more thing – data value. Even if you never see a charge, the information you surrendered has utility to someone else. Names, emails, usernames, and passwords fuel credential-stuffing attempts later. Device IDs and location data expand the profile. Your win condition is minimizing exposure and hardening anything tied to the email you used. That means unique passwords, two-factor authentication, and a hard rule against recycling credentials used during speculative signups.

Let’s recap the non-negotiables. Treat the $100 signup carrot as a red flag, not a reward. Treat the $50 per referral line as fantasy financing. Treat counters without audits as wallpaper. Treat missing support and hidden ownership as deal breakers. Treat an inability to verify referrals – no names, no emails – as structural opacity. Treat legalese without transparency as decoration that changes nothing.

If you’ve already engaged, you’re not stuck – you’re early. Lock down passwords. Turn on two-factor. Review financial apps. Save evidence. Report links. Then warn anyone you invited. That last step matters because the system leans on your reputation to spread. Breaking that chain protects people who trust you.

Bottom line

This proposition is the same tune played on a shinier instrument. Big promises, tiny proof. A trust signal scraping the floor. A domain reported as newborn. Hidden ownership. Missing support. Testimonials that don’t tie to real people. Direct accounts of balances that won’t cash out, like that $304 frozen on a dashboard that refuses to release funds. When headline numbers collide with vanishing evidence, you’re looking at a mirage. Treat it like one. Block, ignore, move on, and keep your accounts locked tight.